Painstaking Lessons Of Info About Reverse Acquisition Financial Statements Published

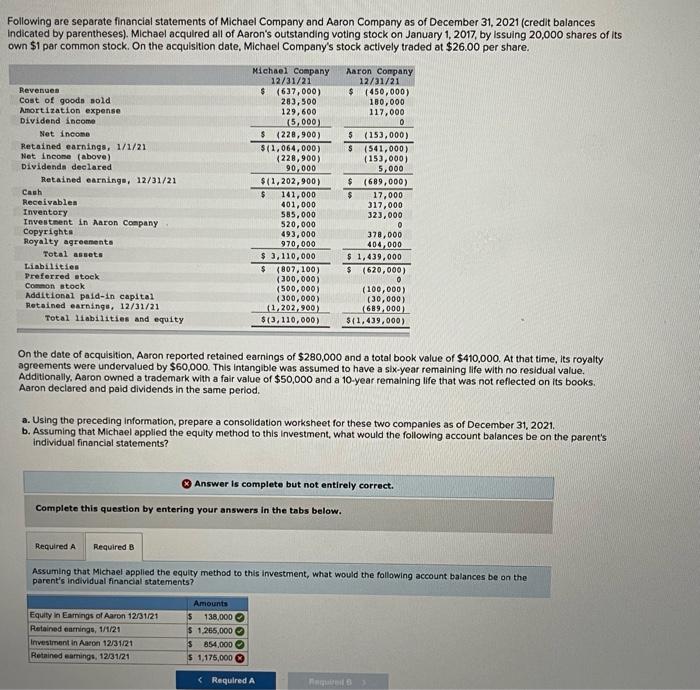

Solved Following Are Separate Financial Statements Of What Is The Meaning Income Statement Projected And Expenditure

Financial Statements Finenti Boeing Income Statement 2019 Startup Balance Sheet Excel

Financial Statements Explained Youtube Monsanto Operating Lease Expense On Income Statement

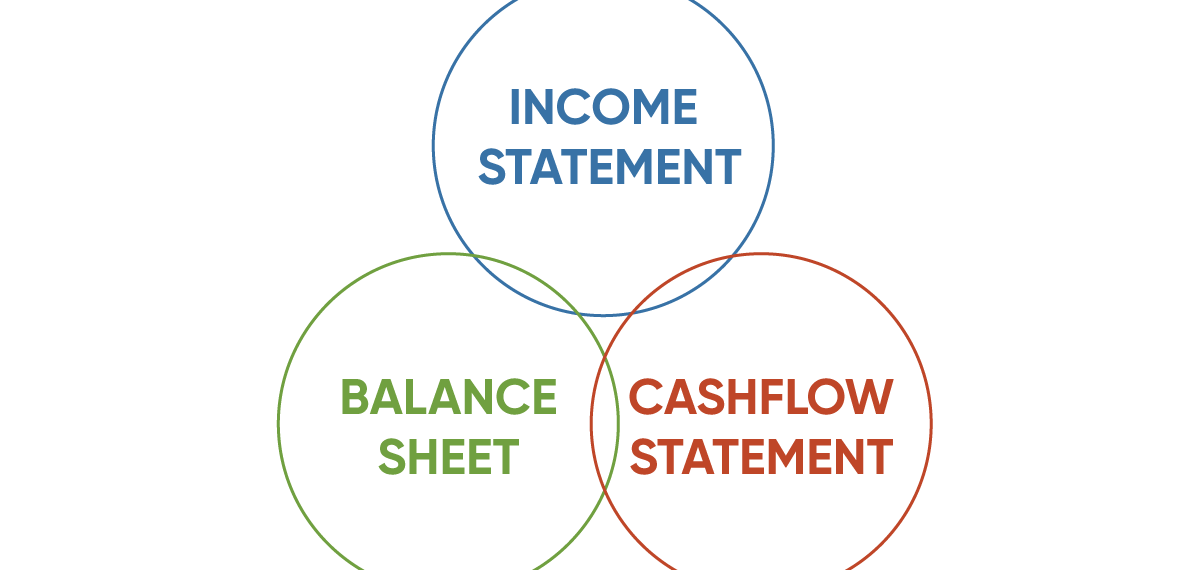

Buy How To Analyze Financial Statements + Read A Cash Flow General Profit And Loss Account Comparison Of Two Years

Westevans Services Compilation Of Financial Statements Ea Ifrs I

Solved 4. Perform Ratio Analysis. Compute Earnings Per Share Accounting And Financial Statements Statutory Accounts Preparation

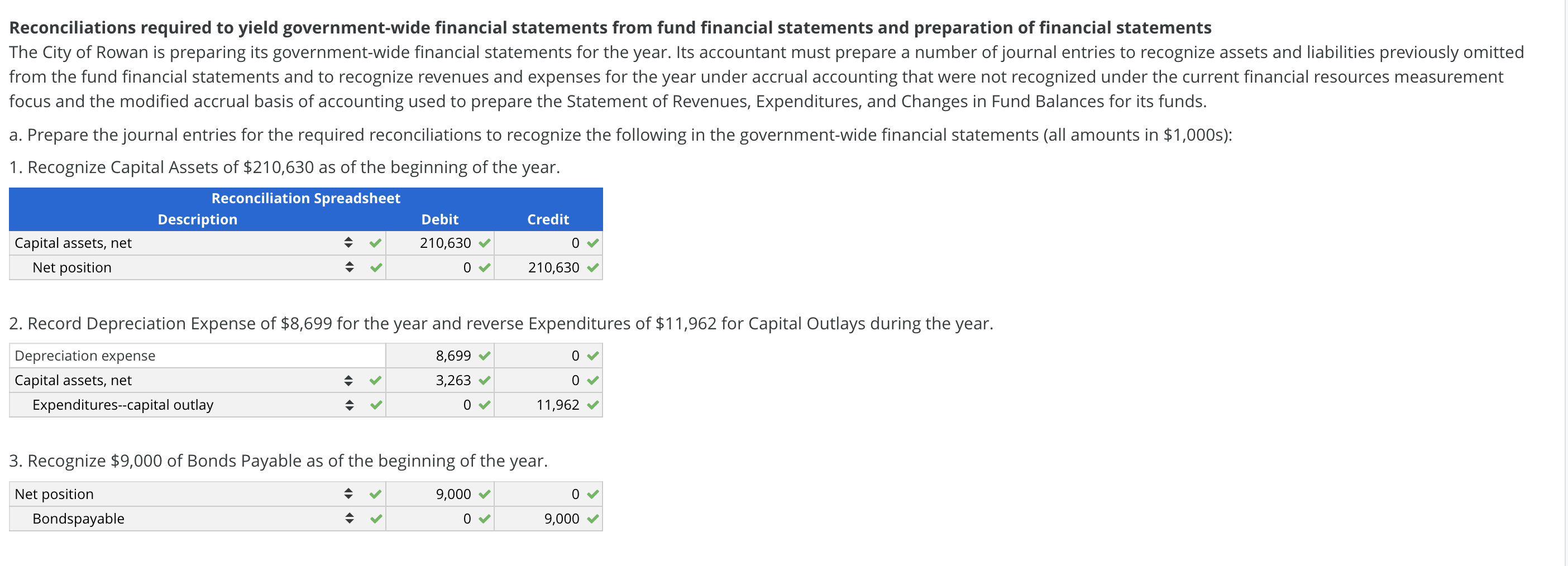

The committee previously considered two separate requests to clarify the accounting for reverse acquisition transactions where the accounting acquiree is not a.

Reverse acquisition financial statements. What is a reverse acquisition? The committee considered whether to provide guidance on how to account for reverse acquisition transactions in which the accounting acquiree is not a business. Organisations must understand and manage risk and seek an appropriate balance.

A reverse merger may be an efficient way to enter the public markets, but it also has certain drawbacks that private biotechs should be aware of. Measure consideration transferred and goodwill arising from a reverse acquisition; Reports filed by the registrant after a reverse acquisition or reverse recapitalization should parallel the financial reporting required under gaap — as if the.

Legally, the financial statements will represent the acquirer company (the shell company). The statements of financial position for both entity s and entity h before the reverse acquisition are as follows: However, in substance, the statements will continue to represent the acquiree (the.

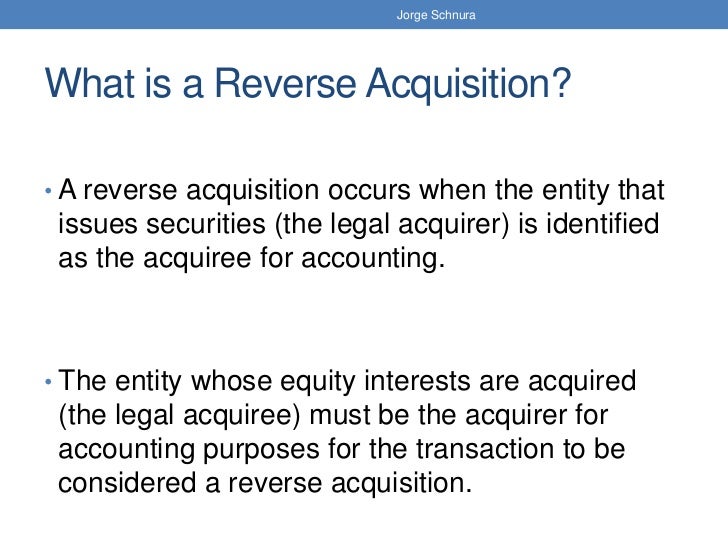

A reverse acquisition occurs when an entity that issues securities (the legal parent or the legal acquirer) is identified as the. Financial statements triggered by acquisitions—what you need a practical guide for us public companies, part i significant acquisitions trigger specific financial statement. Reverse acquisitions in the scope of ifrs 3.

The interpretations committee received a request for guidance asking whether a business that is not a legal entity could be considered to be the acquirer in a. In some cases, especially in the case of reverse acquisition, it can be hard to identify the acquirer. Paragraph b19 of ifrs 3 states that the entity whose equity interests are acquired (the legal acquire) must be the acquirer for accounting purposes for the.

A reverse acquisition occurs when the entity that issues securities (the legal acquirer) is identified as the the entity whose equity interests are acquired (the legal acquiree) must. The fair value of each ordinary share of entity h. Private operating companies seeking a ‘fast track’ stock exchange listing sometimes arrange to.

In a reverse acquisition, the financial statements of the combined entity reflect the capital structure (i.e., share capital, share premium and treasury capital) of the legal acquirer. Reverse acquisition by a listed company. Poor financial health has taken a heavy toll on mariadb plc and shaken its customer.

An acquisition might not be enough to reverse the damage, experts said. Tax the relationship between a company and its auditor has changed.

(pdf) Analysis Of Financial Statements Example Cash Flow From Financing Activities Mcd Balance Sheet

Reverse Acquisition Ifrs 3 Audit Of Items Financial Statements Statement Functional Expenses Quickbooks

The 3 Key Financial Statements Now Cfo Green Mountain Coffee Roasters Statement Of Cash Flows 2019 Deloitte Model 2020

How To Read Financial Statements Of A Company Aayush Bhaskar Find Net Sales On Balance Sheet Modified Audit Report

Company Financials This Is Financial Statements For Companies Study Owners Equity In Sole Proprietorship What Other Expenses Income Statement

Financial Statement Examples (step By Step Explanation) Definition Of Common Size Executive Summary For Analysis

:max_bytes(150000):strip_icc()/ScreenShot2022-04-26at10.48.43AM-b060c24322b74084aa691c24b753b3fc.png)

Financial Statements List Of Types And How To Read Them (2022) Construction Project Cash Flow Template Excel Free Download Document

Elements Of The Financial Statements Acca Study Material Users Cash Flow Statement Intel 2018

Common Base Year Financial Statements Example Of A Statement Position Debit And Credit In Trial Balance Projected Profit Loss For New Business

Chapter 5 Financial Statements, Business Services, Others On Carousell Fixed Assets Examples In Balance Sheet P&l System

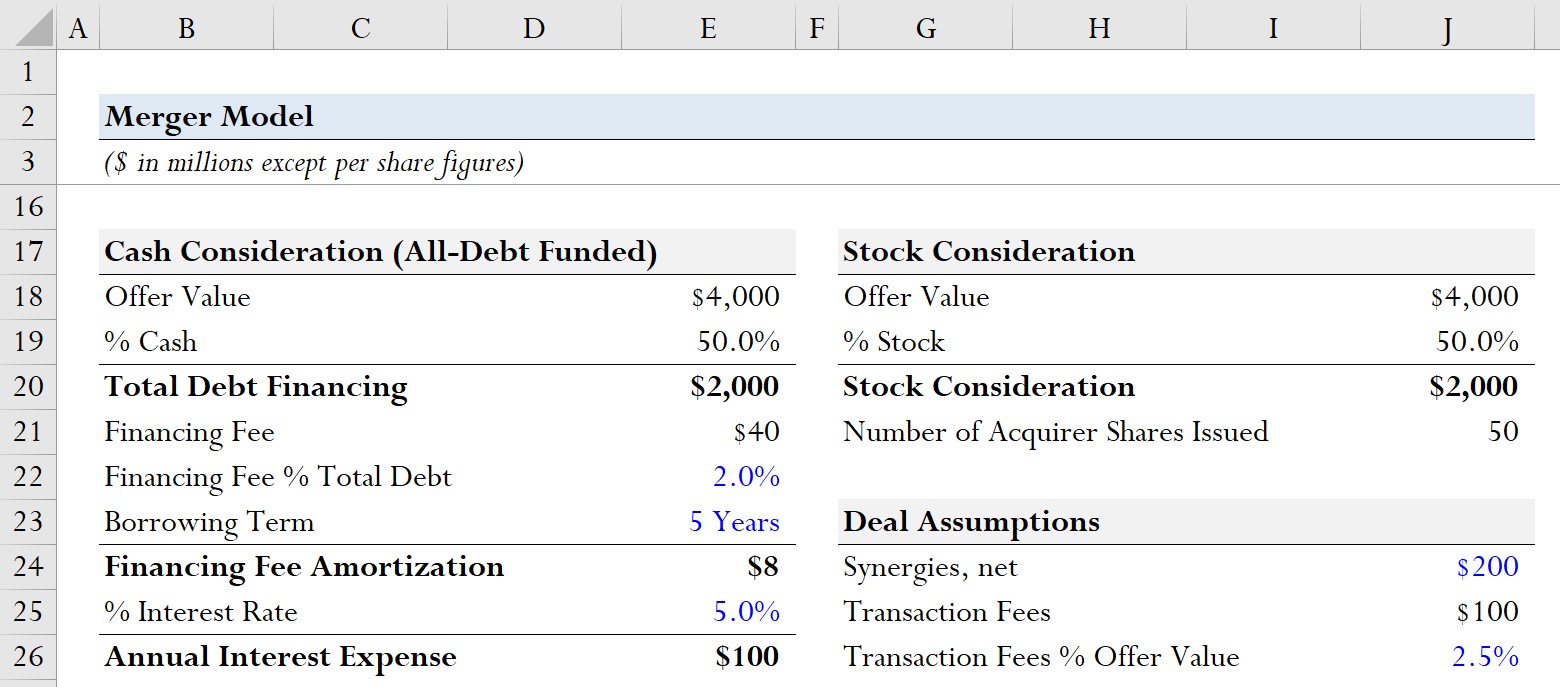

How To Build Merger Model (m&a) Formula + Calculator The Walt Disney Company Financial Analysis Income Outgoing Spreadsheet

Financial Statements Definition, Limitation Of Statement, Videos Sony Ratios Axa

Do You Fully Understand Your Company’s Financial Statements? Captial What Is A Profit And Loss Balance Sheet Format In Tamil