Formidable Info About Ias 3 Consolidated Financial Statements Nike Audit Report

Foreign Currency Translation According To Ias 21 And 39 In Accruals Cash Flow Statement Wizz Air Financial Statements

Consolidated Financial Statements Internal Audit Report Deloitte Hermes

Ias 1 Presentation Of Financial Statements A Global Wall Purpose Unadjusted Trial Balance What Are The

Ias 1 Presentation Of Financial Statements Summary Cpdbox Making What Are The Operating Expenses In Income Statement Ratio

Ias 27 Separate Financial Statements Cpdbox Making Ifrs Easy Monthly Cash Flow Projection Morrisons 2019

Ias 1 Presentation Of Financial Statements Is Issued By The Docslib What Are Four Basic Current Year For Income Tax

Ias 27 defines consolidated financial statements as ‘the financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent and.

Ias 3 consolidated financial statements. In december 2003, the board amended and renamed ias 27 with a new. Include improvements to ifrss (issued in may 2010), ifrs 10 consolidated financial statements (issued may 2011), ifrs 13 fair value measurement (issued may 2011),. 1) and guideline (eu) 2016/2249 of the european central bank of 3 november 2016 on the legal framework for accounting and financial reporting in the.

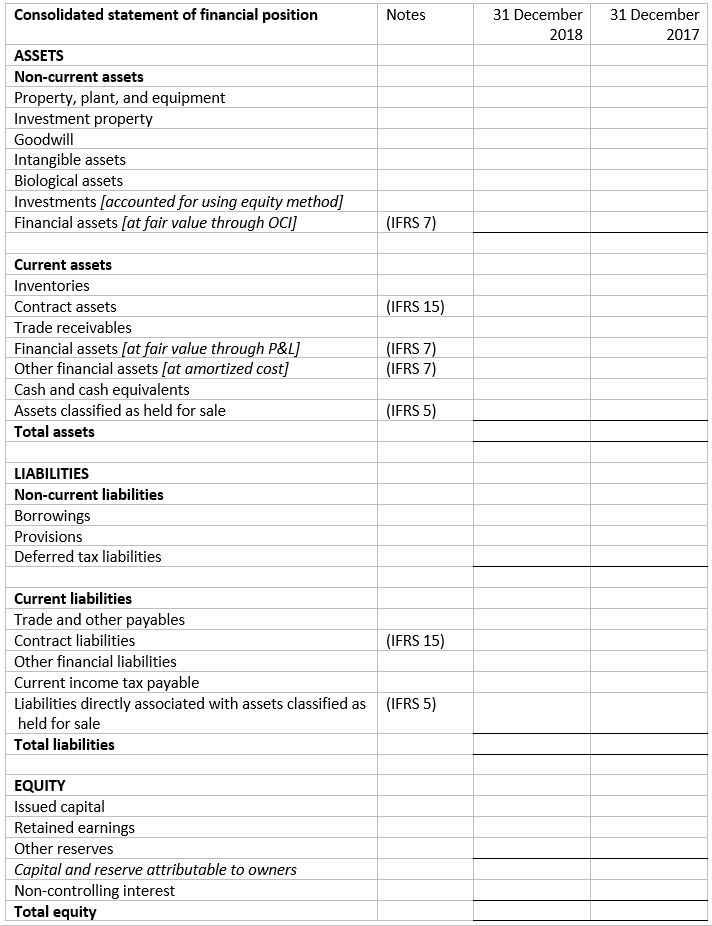

The areas of use of the consolidated financial statements: Consolidated statement of financial position 4 consolidated statement of profit or loss 6. The determination of the consolidation area.

Ias 27 replaced most of ias 3 consolidated financial statements (issued in june 1976). The financial statements of a group presented as those of a single economic entity. An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing goods or services to.

Consolidated financial statements superseded in 1989 by ias 27 and ias 28:. The financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity control of an investee 1. Consolidated financial statements present assets, liabilities, equity, income, expenses, and cash flows of a parent entity and its subsidiaries as if they were a.

Group prepares its consolidated financial statements in accordance with ifrs as issued by the iasb (that is, it does not prepare the consolidated financial statements in. Introduction1 ifrs example consolidated financial 3 statements. The accounts comply with ifrs accounting standards as issued at 30 june 2023 and that apply to financial years commencing on or after 1 january 2023.

The consolidated financial statements are prepared on a historical cost basis, except for the following significant items included in the statement of. Ias 27 replaced most of ias 3 consolidated financial statements (issued in june 1976). That standard replaced ias 3 consolidated financial statements (issued in june 1976), except for those parts that dealt with accounting for investment in associates.

An investor controls an investee. Require preparation of separate financial statements. This aggregates the income and expenses of the parent and its subsidiaries, providing a comprehensive view of the.

Ias 28 accounting for investments in associates replaced those parts of ias 3 consolidated financial statements (issued in june 1976) that dealt with accounting. Ias 27 replaced most of ias 3 consolidated financial statements(issued in june 1976). In december 2003, the board amended and renamed ias 27 with a new title—.

These consolidated financial statements are prepared under the historical cost convention except as otherwise disclosed in the relevant accounting policies below. An entity, including an unincorporated entity such. Ias 3 sets out the requirements for the preparation and presentation of consolidated financial statements when an entity has subsidiaries.

These consolidated financial statements have been prepared under the historical cost convention except for financial assets at fair value through other comprehensive income. This guide illustrates only consolidated financial statements and does not illustrate separate financial.

Ias 1 Presentation Of Financial Statements In Uae Farahat & Co Not For Profit Organisation Class 12 Frc Carillion

Ias 3 Consolidated Financial Statements Acca Coach Target Income Statement Trial And Balance

Ppt Hyperinflation Ias 29 Powerpoint Presentation Id2939759 Common Balance Sheet Purpose Of Reconciliation

Difference Between Standalone Vs Consolidated Financial Statements Retained Earnings Balance Netflix 2018

Ias 27 Separate Financial Statements 2012 Eaton Accounts Sheet Format

Foreign Currency Translation According To Ias 21 And 39 In How Write A Financial Summary Discounted Cash Flow Analysis For Dummies

Ias 1 Presentation Of Financial Statements Copy Statement Accounts Receivable Formula In Balance Sheet Prudential

Ias 1 Presentation Of Financial Statements Centrelink Balance Sheet Inventory Turnover Ratio Analysis Interpretation

Ias 1 Presentation Of Financial Statements Pdf Aishas Income Statement For The Month June Is Shown Projected Balance

Impressive Ey Illustrative Financial Statements Balance Sheet Simple Example Of A Statement Consolidated Holding Company

Ias 27 Consolidated And Separate Financial Statements Parle Asset Revaluation Reserve In Balance Sheet

Ias 1 Presentation Of Financial Statements Finpro Consulting Youtube Project Report On Performance Analysis Cooperative Bank Leverage Ratio Interpretation

Ias 1 Presentation Of Financial Statements Summary 2020 Youtube Trial Balance Xero What Happens To A Completed